Description

Lesson 1: Definition and Purpose of EWRA

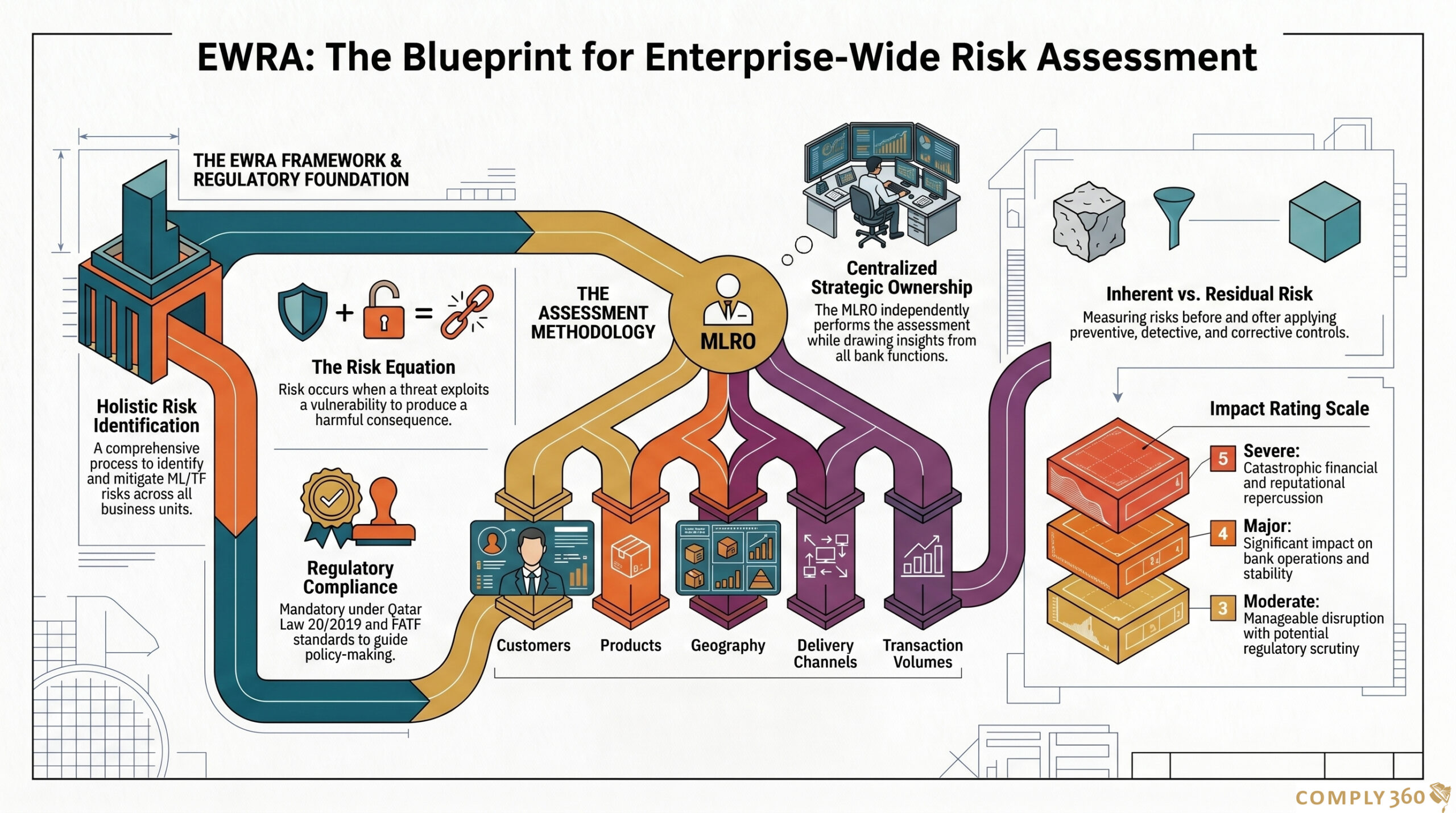

- Definition: EWRA is a strategic and comprehensive process used by financial institutions to identify, assess, and mitigate money laundering (ML) and terrorist financing (TF) risks across the entire organization.

- Purpose: It periodically evaluates potential risks across all business units, products, services, customer types, and geographic locations.

- The Risk Equation: Risk occurs when a threat (a person or group with harmful intent) takes advantage of a vulnerability (inherent features of a product or sector) to produce a consequence (harm to the financial system or society).

Lesson 2: Regulatory Requirements for EWRA

- Primary Law: Requirements are anchored in Law 20/2019, which details articles on customer due diligence, risk management, and internal controls.

- Implementing Regulations: These set specific obligations for regulated entities to assess risk and perform enhanced due diligence for higher-risk activities.

- Specific Jurisdictions: For entities within the QFC zone, compliance with the QFC AML/CFTR Rules is mandatory.

Lesson 3: Role of the Compliance Department

- Strategic Ownership: The Money Laundering Reporting Officer (MLRO) is responsible for independently performing the EWRA using the bank’s compliance governance framework.

- Centralization: While tactical mitigation may be delegated to business units (first line of defense), the overall strategic assessment is centralized under the Compliance Division.

- Key Responsibilities: Compliance ensures regulatory alignment, conducts training and awareness, and manages the ongoing monitoring and review of risks.

Lesson 4: Assessment of Risks (Inherent and Residual)

- Inherent Risk: This is the “natural” risk level present in a customer, product, or transaction before any controls are applied. It is determined by factors such as customer type, business activity, and geographic location.

- Vulnerability Assessment: Identifying vulnerabilities requires analyzing the size and complexity of business lines, the types of customers engaged, and the methods of service delivery (e.g., online vs. in-person).

- Residual Risk: This is the remaining risk exposure after accounting for the effectiveness of management controls.

- The Formula: Inherent Risk ± Controls = Residual Risk.

Lesson 5: Structured Data-Driven Risk Scoring Methodology

- Expert Judgment: Inherent risk scoring is grounded in professional judgment, subject matter expertise, and institutional knowledge rather than just numerical data.

- Rating Dimensions: Risks are rated based on their Likelihood (probability of occurrence) and Impact (magnitude of severity).

- Scoring Scales: Likelihood is rated from 1 (Rare) to 5 (Almost Certain), while Impact is rated from 1 (Insignificant) to 5 (Severe).

Lesson 6: Documentation and Reporting of EWRA Results

- Core Outputs: The EWRA process generates a Risk Assessment Report, a Risk Mitigation Plan, a Risk Register/Heat Map, and a Board/Management Summary.

- Board Oversight: Final results are presented annually to the Board Audit, Risk & Compliance Committee for acknowledgement.

- Application of Results: Findings are used to design triggers, red flags, and scenarios for account monitoring, ensuring high-risk customers receive deeper scrutiny

Reviews

There are no reviews yet.